Mortgage Rates Today: The Breakthrough Insights You Need for Your Future

Okay, folks, let’s dive into something that’s been weighing on a lot of minds lately: mortgage rates. I know, I know, finance isn't usually the stuff of dreams, but trust me, there's a spark of optimism here that we can't ignore.

A Shift in the Wind?

So, the headline is this: mortgage rates are mostly down a smidge this week, according to Bankrate. We're talking about a 6.28% average for a 30-year fixed, which is a teeny, tiny 0.04% dip from last week. The 15-year fixed and 5/1 ARM are also down. Now, before you start planning that mansion, remember that 30-year jumbo loans did tick up a bit. But still, the overall trend? Downward. And that, my friends, is a reason to perk up.

Why? Well, it’s like this: imagine the economy is a garden. High interest rates are like a drought, making it tough for anything to grow. A slight dip in rates? That's like a little rain shower. It doesn't solve everything, but it gives those little seedlings—new homebuyers, folks refinancing—a chance to breathe a bit easier.

And speaking of breathing easier, I can’t help but think about what Mark Hamrick from Bankrate said: Americans are feeling the squeeze with inflation and job market worries. He’s right, of course. But here’s the thing: even a potential rate cut in December, as hinted by New York Fed President John Williams, is enough to send ripples of hope through the financial markets. It might not "make or break" households, as Hamrick notes, but the anticipation of relief is powerful. It's a signal that things could get better.

Now, the real kicker is the 10-year Treasury yield sliding to its lowest this month. That's essentially the bond market whispering that it expects interest rates to fall. Is it a guarantee? Absolutely not. But it’s another sign pointing in the same direction. What does this mean for us? What could it mean for you?

Here's a question I've been pondering: if the Fed does cut rates in December, how quickly will that translate into actual savings for homeowners and buyers? Will lenders be eager to pass those savings on, or will they hold onto them for a bit, citing other factors? It's a question worth asking.

A Reason to Believe

Look, I get it. We’ve been bombarded with doom and gloom for months. But this tiny dip in mortgage rates? It's a reminder that the economic landscape is constantly shifting. It's not a fixed, immutable thing. It’s a dynamic, breathing entity, and right now, it seems to be exhaling just a little bit of relief. This is the kind of breakthrough that reminds me why I got into this field in the first place.

Of course, we need to be realistic. As Hamrick pointed out, people are still facing challenges. But sometimes, all it takes is a glimmer of hope to keep us going. And that’s precisely what this slight downward trend offers: a reason to believe that things can, and will, get better.

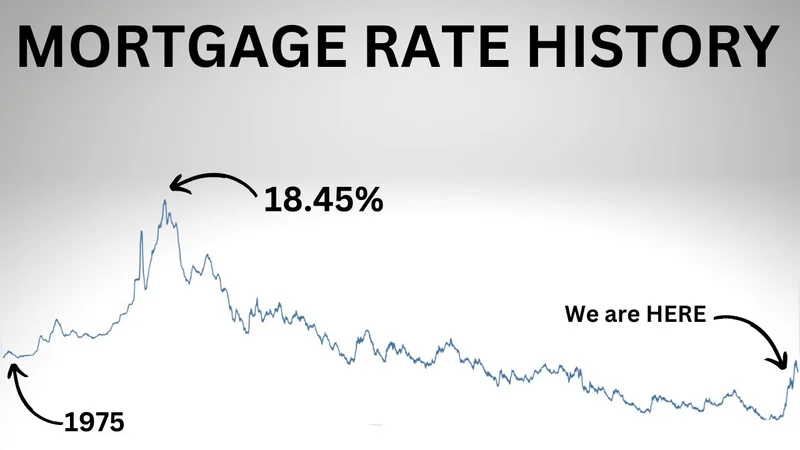

Now, let's not get carried away. We're not talking about a return to the rock-bottom rates of a few years ago. But remember, today's rates are still significantly lower than the 40-year average of 7.2%. So, perspective matters. It's all about perspective.

And hey, speaking of perspective, what if this is the start of a larger trend? What if this small dip is the first domino to fall, leading to more significant rate cuts down the line? I know, I know, I'm getting ahead of myself. But a guy can dream, right? That is how innovation happens, after all.

The Dawn is Coming

Mortgage rates dipping? It's more than just numbers; it's a whisper of hope that brighter days are ahead.